The EU’s direction in the post-quota era

The EU is adjusting to life without production limits. Milk supply growth has been strong to date, particularly in low-cost regions of Ireland, the Netherlands and Germany. Farmgate prices haven’t fully reflected the wild ride in wholesale quotes, as the large stable domestic market buffers producers. Is the EU expanding its productive potential to assume a larger slice of global trade, or are these the early months of a wild ride?

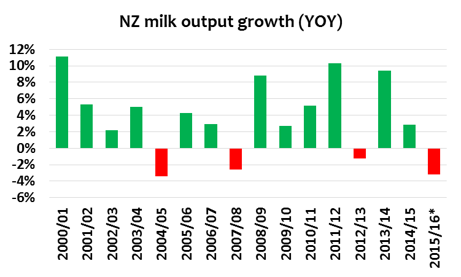

NZ farmers staring at their 3rd poor year

NZ milk output has been buffeted by low farmgate prices and poor weather, but not nearly as much as some expected. But weather patterns are erratic. Rain and soil moisture have improved the short term milk response, particularly on the South Island. The prospect of deeper cash losses will again limit output in 2016, especially as farmers face a third season at sub-NZ$5/kg milk prices. New Zealand grew strongly on the promise of Chinese demand, but now that the bubble has burst, where to next?

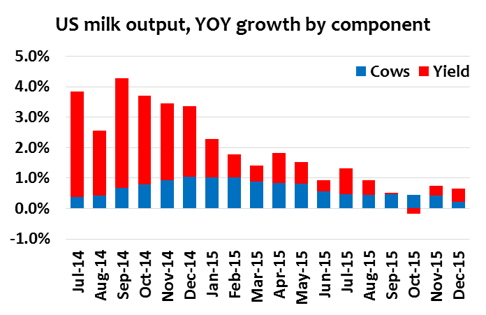

US milk supply remains resilient

Milk production growth in the US remains in expansionary mode, despite cycles in farm prices and margins. The US remains a finely balanced story, but with extremely different regional situations. Milk expansion seems assured, but with relatively flat domestic demand, the industry must come to terms with effectively competing – in innovation, cost and service – to grow its share of the global market.

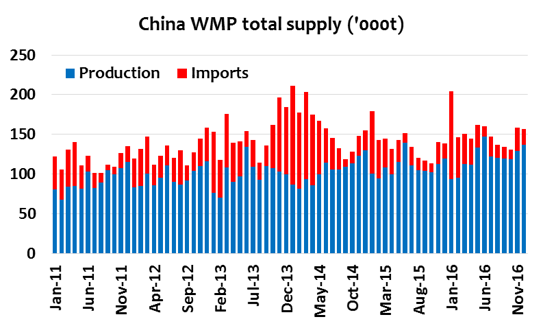

What is really happening in China?

Financial market turbulence overflow into the new year has raised major concerns about the ability of policy makers to manage the economy’s transition into the medium term. With consumer confidence and purchasing power key to broader growth in dairy demand, it seems the industry is gearing up local supply of WMP but consumption preferences will continue to evolve and provide diverse opportunities. Data is mostly anecdotal, but our DTS allows assumed growth in imports to be assessed in the context of wider developments.

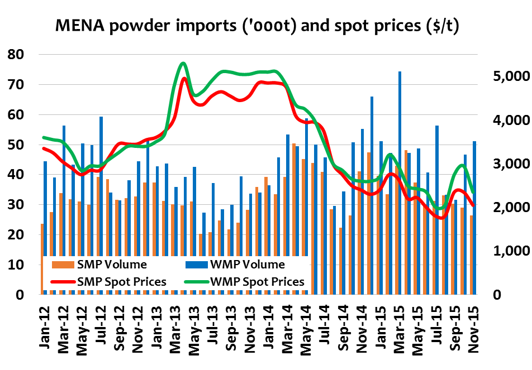

When will price-sensitive regions rebound?

Supply chain pipelines filled in 2015 for many price sensitive markets as buyers took advantage of low prices. Some however remain spot buyers in a wash market. Trade statistics across these regimes show a variety of trends, but generally add-up to mean global dairy prices will remain grounded for the time being. Will low prices spur stronger buying to ignite a recovery?

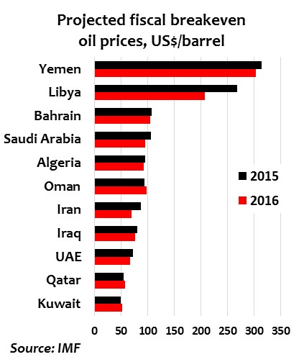

Low oil prices – can buyers afford dairy?

The outlook for global oil prices has worsened in recent months, with low prices being a new normal for the foreseeable future. Dairy buyers in major oil exporting countries will be hit, but some more so than others. There are dangers in generalising the effects on dairy imports. The effect will be uneven, depending on a number of factors that affect spending on dairy foods which vary markedly. These include the oil-production break-even points; economic dependence on crude oil production; oil incomes as a portion of government revenues; the scale of government food purchasing programs; and the financial reserves available to weather the effects of an oil glut over time.

Demand in home markets

Drinking milk consumption has been falling in both home markets of the EU and US as a longer-term trend, but cheese demand is improving particularly in the US where foodservice performance has been spectacular in 2015. The weaker Eurozone economy faces stronger challenges and if this weakens cheese demand, more milk will head for exports. These developments are critical to the outlook for the world market.

How long will feed prices stay low?

Feed supplies are plentiful due to good weather. In the US, combined corn and soybean inventories were reported as highest ever. In the short-term, with downward pressure on farmgate prices expected in the US and EU, cheap feed will ensure margins stay in tact, ultimately prolonging any global dairy price recovery.

Source: FreshAgenda